How to Get Affordable Auto Insurance in Quebec After Tickets, Claims or Cancellations

You open your renewal letter or check a new quote and the price stops you cold. It is significantly higher than you expected. You might even be facing a decline letter from a standard insurer.

This moment creates a specific kind of anxiety. It is not just about the money. It is the feeling of being trapped. You worry that a past mistake has permanently locked you out of the affordable market. You worry that you are now labeled "bad business" and will be forced to overpay forever.

The insurance industry often relies on this anxiety. When you feel powerless you are less likely to shop around. You are more likely to accept a punishing rate because you believe you have no other choice.

This belief is false.

You are not uninsurable. You are simply navigating a temporary period of "Rate Adjustment." This is a mathematical status, not a moral judgment. It has a specific start date and a specific end date. More importantly, it has a solution.

At Panda7 we do not believe in penalty boxes. We believe in recovery plans.

This guide is your technical roadmap back to standard rates. We will dismantle the "High Risk" label and show you exactly how insurers calculate your surcharge. We will map out the timeline for when your record heals. We will give you the specific levers you can pull today to lower your payments immediately.

Most importantly we will show you how to access the "Specialty Market" carriers that actually want your business.

Key Takeaways: Your Recovery Playbook

The "High Risk" Myth: You are likely not uninsurable. You simply need a "Specialty Market" insurer (like Intact Solution or Pafco) who uses a different pricing model than the big banks.

The 3-Year Rule: Most major infractions like non-payment cancellations impact your rate for exactly 3 years. After that, they disappear from your rating entirely.

The Reinstatement Fix: If you were cancelled for non-payment recently, paying the balance immediately can sometimes reverse the cancellation. Always try this first.

The "One-Way" Lever: Dropping collision coverage on an older car is the single fastest way to cut a high-risk premium in half.

The Recovery Path: Your road back to standard rates is built on 12-month increments. Every year of clean payments and safe driving lowers your "reliability score" and your price.

Phase 1: The Diagnostic (Understand Your Status)

To fix the problem you must first define it accurately. "High Risk" is a lazy industry term that lumps everyone together. In reality your specific situation dictates your price and your recovery speed.

Insurers use a central database called the Fichier Central des Sinistres Automobiles (FCSA) to track your history. They also check with the SAAQ. Different entries on these records trigger different surcharges.

Identify your scenario below to understand the real impact on your wallet.

Scenario A: Cancellation for Non-Payment

- The Reality: You missed payments. The insurer sent a registered letter. The policy was cancelled.

- The Impact: This is a major red flag for insurers because it predicts financial instability. It typically results in a surcharge of $1,500 to $3,000 per year [Source: Panda7 Market Data].

- The Duration: It remains on your file for 3 years [Source: GAA].

- The Recovery: The surcharge is heaviest in Year 1. If you maintain perfect payments with a specialty insurer for 12 months you can often negotiate a lower rate in Year 2. By Year 3 the impact is minimal.

- Crucial Tactic: If this happened recently (last 30-60 days) ask about "Reinstatement." Paying the balance immediately can sometimes force the insurer to reverse the cancellation entirely. This wipes it from your record as if it never happened.

Scenario B: The At-Fault Accident

- The Reality: You caused a collision. The insurer paid out a claim.

- The Impact: A single at-fault accident typically raises premiums by 30% to 50%. Two at-fault accidents in 5 years may get you declined by standard markets entirely.

- The Duration: It impacts your rating for 6 years in Québec.

- The Recovery: The impact fades over time. A 5-year-old accident costs you less than a 1-year-old accident.

Scenario C: The License Suspension

- The Reality: Your license was suspended by the SAAQ for demerit points or unpaid fines.

- The Impact: Insurers view this as a disregard for the rules. It often triggers a surcharge of 50% to 100%.

- The Duration: The suspension stays on your driving record for 6 years even after you get your license back.

- The Recovery: You must demonstrate strict adherence to the rules. Combining this with a telematics app is the fastest way to prove you have changed your habits.

Scenario D: Criminal Convictions (DUI)

- The Reality: A conviction for driving under the influence.

- The Impact: This is the most severe category. You will likely be moved to the "Non-Standard" market immediately. Premiums can double or triple. For example a $1,000/year base rate could become $4,000 or more.

- The Duration: A DUI conviction impacts insurance for up to 10 years.

- The Recovery: Recovery is slower here but still possible. It requires absolute consistency in maintaining a clean record moving forward.

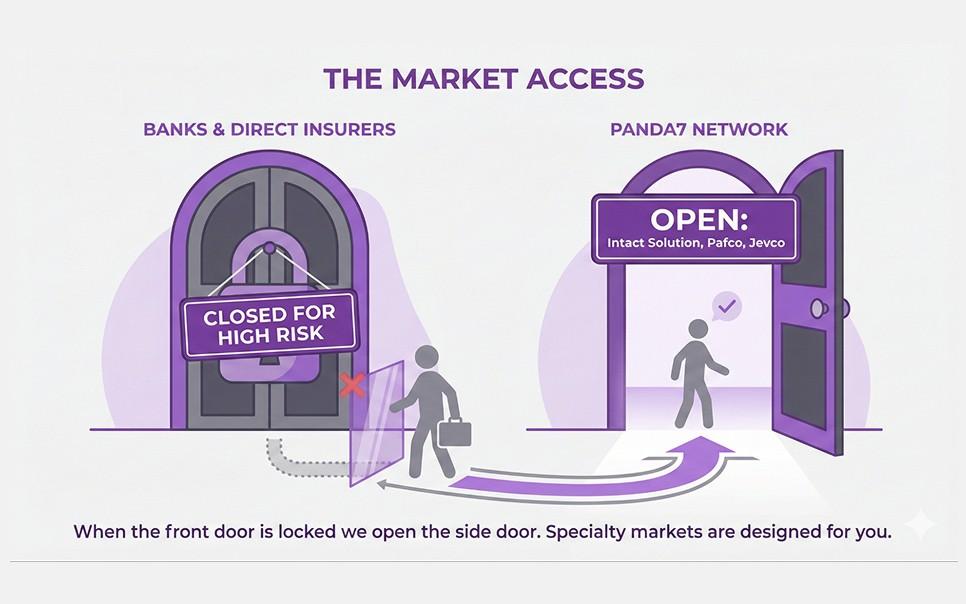

Phase 2: The "Specialty Market" Solution

You might have been told by a bank or direct insurer: "We cannot insure you." Translation: "We do not have a product for you."

Standard insurers (the ones with big TV ads) operate like cookie-cutter factories. They want identical low-risk clients. If you do not fit the mold they reject you.

Panda7 operates differently. We work with Specialty Market Insurers.

Who Are These Insurers?

These are divisions of major companies specifically designed for complex profiles. They do not use a cookie cutter. They use a custom mold.

- Intact Insurance "Solution Program": A dedicated division for drivers with cancellations or minor convictions.

- Pafco: A specialist insurer for drivers who need a second chance.

These companies expect to see cancellations and tickets. They price for it fairly and give you a valid policy. They are fully regulated and offer the same protections as standard insurers.

Phase 3: Your Recovery Roadmap

You need a plan. You need to know when this ends. Here is the standard recovery timeline for a driver with a non-payment cancellation or multiple infractions.

Step 1: Immediate Stabilization (Month 0)

- The Action: Secure a policy with a specialty insurer immediately.

- The Strategy: Do not drive uninsured. Even a one-day gap creates a "ratable lapse" that increases your price further. Accept the higher rate as a temporary bridge. Set up automatic payments to ensure you never miss a deadline.

- The Goal: Stop the bleeding. Get legal. Start the clock on your clean history.

Step 2: The Telematics "Correction" (Month 1)

- The Action: Enroll in a program like Intact myDrive.

- The Strategy: Your past says you are risky. Telematics proves you are safe today.

- The Math: A high safety score can earn you a 25% discount. This directly offsets your surcharge. It is the fastest way to prove the algorithm wrong.

Step 3: The First Review (Month 12)

- The Milestone: You have completed one full year of on-time payments.

- The Action: Panda7 automatically reviews your file 30 days before renewal.

- The Result: Because you have proven financial stability for 12 months your "reliability score" improves. While you may still be with a specialty insurer your surcharge often drops by 10% to 20%.

Step 4: The Transition Zone (Month 24)

- The Milestone: Two years of clean history.

- The Action: We re-shop your profile against "Standard Market" insurers.

- The Result: Some forgiving standard insurers may now accept you. If not, your specialty rate continues to drop. You are now paying significantly less than Day 1.

Step 5: Full Recovery (Month 36)

- The Milestone: The 3-year mark (for cancellations).

- The Action: The cancellation for non-payment falls off your record completely [Source: GAA].

- The Result: You are eligible for standard rates again. You have crossed the finish line. Your premium returns to the baseline for your age and vehicle.

Phase 4: Tactical Steps to Lower Your Rate NOW

You do not have to wait 3 years to save money. Even with a "Temporary Rate Adjustment" you have levers to pull today.

1. The "One-Way" Lever

If you drive an older car consider dropping Collision coverage entirely.

- The Strategy: Carry "One-Way" (Civil Liability) only.

- The Math: This removes the cost of repairing your car. For a high-risk profile this portion of the premium is huge. Removing it can cut your bill in half.

- The Safety Net: In Québec if you are hit by a driver who is 100% at fault you are still covered under Direct Compensation even with One-Way coverage.

2. The Deductible Lever

High-risk insurance is expensive. To lower the monthly bill you must take on a little more risk yourself.

- The Strategy: Raise your Collision Deductible to $1,000 or even $2,000.

- The Math: This can drop your premium by 15% to 20%. You are betting on yourself. It puts money back in your pocket every month.

3. The Payment Rehabilitation

If your issue was non-payment you must rebuild your financial credibility.

- The Strategy: If possible pay your full annual premium upfront.

- The Benefit: This eliminates the risk of another missed payment. It often secures a "Paid in Full" discount. It proves to the insurer that you are solvent and serious.

4. Optimize Your Coverage Menu

Just because you are high-risk does not mean you should pay for fluff. Audit your policy for these extras.

- Rental Car Coverage (QEF 27): This covers you when you rent a car. If you don't travel often remove it to save $40-$60/year.

- Courtesy Car (QEF 20): This gives you a rental if your car is in the shop. If you have a second car or can take the bus consider dropping it to save $30-$50/year.

- Replacement Cost (QEF 43): If your car is older than 5 years ensure this expensive endorsement is removed. You don't need to insure the "new" value of an old car.

Expert Answers to Your Recovery Questions

How long does a non-payment cancellation stay on my record?

In Québec a cancellation for non-payment remains on your file for 3 years from the date of cancellation [Source: SAAQ/GAA]. However the financial impact is most severe in the first 12 to 24 months. By the third year if you have maintained continuous coverage the surcharge drops significantly.

Can I fix a cancellation by paying what I owe?

Yes sometimes. This is called "Reinstatement." If you receive a cancellation notice you typically have a window (often 15 to 30 days) to pay the full outstanding balance. If you do this the insurer may agree to "reinstate" the policy without a lapse. This completely erases the cancellation from your record. It is always worth trying this first.

What is the difference between the SAAQ contribution and my private insurance premium?

You pay for insurance in two places.

- SAAQ Contribution: Paid when you renew your driver's license. Covers bodily injury. Cost increases based on your demerit points (e.g. 4-9 points = roughly $160-$400 surcharge).

- Private Premium: Paid to Panda7. Covers property damage. Increases based on your risk profile (accidents, cancellations). Both will go up with a bad record but they are calculated separately.

Am I in the "Facility Association"?

If you are in Québec the answer is No. The "Facility Association" is for Ontario and other provinces. In Québec we have the Risk Sharing Plan (RSP) managed by the GAA. It is a pool for the highest-risk drivers. However your Panda7 broker works to keep you out of the RSP by finding a private specialty insurer (like Intact Solution) first which is almost always cheaper.

If I hide my past cancellation will the new insurer find out?

Yes absolutely. Insurers use a central database called the Fichier central des sinistres automobiles (FCSA). Every claim and cancellation is recorded there. If you lie it is "Material Misrepresentation." This can void your policy retroactively (meaning they won't pay any claim) and get you blacklisted. Honesty is the only path to a valid policy.

Does taking a defensive driving course help lower my rate?

It can. While it won't erase a cancellation it sends a positive signal. Most insurers focus on your actual driving history rather than courses. More importantly completing a course combined with 12 months of clean driving is a strong argument your broker can use to negotiate a better rate at renewal.

How do I distinguish between being "Declined" and being "Uninsurable"?

"Declined" means that a specific company doesn't want your risk profile. "Uninsurable" is a myth. In Canada you almost always have access to coverage even if it's through the RSP. If a direct insurer declines you it just means you need a broker to access the specialty market.

Can I switch insurers mid-term if I find a better rate during my recovery?

Yes. You have the unconditional right to cancel your policy at any time in Québec. There is no penalty though you may owe a "short-rate" adjustment (the cost of insurance used + a small admin fee). If the savings on the new policy outweigh this small cost, switching mid-term is a smart move.

What happens if I have a not-at-fault accident on my record?

Unfortunately a not-at-fault accident can still cause your rate to edge up at renewal. While the impact is much smaller than for an at-fault accident insurers consider every claim on your record when setting prices. However it is important to know that even if you only have liability coverage when the other party is 100% responsible your own insurer must still pay for the market value of your vehicle.

Can I still get Accident Forgiveness if I am high risk?

Usually no. Accident Forgiveness is a perk typically reserved for drivers with a clean record (often 6+ years claim-free). Once you are in the high-risk category you lose this protection. This makes driving carefully even more critical as your next accident will impact your rate immediately.

Does bundling help if I am high risk?

Yes it helps immensely. Even if your auto premium is high, bundling it with a tenant or home policy can trigger a Multi-Line Discount of 10-15%. Since the auto premium is large (e.g. $2,000) that 10% saving ($200) is often enough to pay for the entire tenant policy. It is a smart way to get free property coverage while lowering your total bill.

Why do I have to pay upfront?

Insurers view non-payment cancellations as a credit risk. To mitigate this they often require "Payment in Full" for the year or a significant down payment (e.g. 20-30%) for the first term. This is temporary. Once you prove reliable payment history for a year or two you can usually return to standard monthly installments.

Conclusion: Start Your Recovery Today

You now have the map.

You understand that your high rate is a Temporary Adjustment. You know it has an expiry date. You know that you can pull levers like telematics and deductibles to lower it right now.

Most importantly you know that you are not alone.

At Panda7 we do not judge your past. We are here to secure your future. We will help you navigate the "Shadow Market." We will place you with a specialty insurer. We will guide you year-by-year until you are back to standard rates.

Your recovery starts with a single honest quote.

Get Your Personalized Quote & Recovery Plan

You are not "uninsurable." You just need the right partner. Let us find you the specialty insurer that fits your profile and build your roadmap back to standard rates.

Get Your QuoteContinue Your Research

- To learn more about the specific savings strategies available to all drivers read our guide on Provide Actionable Savings Strategies.

- To understand how to audit your policy for value read our guide on Execute a Smart Quote Comparison.

- If you are ready to compare prices immediately use our tool now. Click here.

Data Sources & Methodology: Panda7 is committed to radical transparency.

- Source 1: Autorité des marchés financiers (AMF). Regulations regarding insurance access.

- Source 2: Groupement des assureurs automobiles (GAA). Data on the Risk Sharing Plan and FCSA.

- Source 3: Société de l'assurance automobile du Québec (SAAQ). Demerit points and contribution schedules.

- Source 4: Intact Insurance. Underwriting guidelines for the "Solution" specialty program.

- Source 5: Real-World Case Study. Martin G., Construction Worker from Longueuil. Recovered from non-payment cancellation to standard rates in 28 months (2023-2025).