The Complete Guide to Controlling Auto Insurance Costs in Quebec

Let us be completely honest about how shopping for auto insurance in Quebec usually feels.

It often feels like you are being played by a system designed to confuse you. You spend hours entering your personal information into a website, a random number gets spit out at the end, and you have absolutely no idea how the insurance company arrived at that price. Then, your renewal notice arrives in the mail one year later. Your rate has jumped, even though you have not had a single ticket or filed a single claim. When you try to find out why, you are met with vague answers about "industry trends" or "market adjustments."

It is incredibly easy to feel powerless in this situation. It is even easier to feel suspicious. You start asking yourself the common questions. Am I being ripped off? Is the person living next door paying less money for the exact same coverage? Are there hidden fees buried in this contract?

You are not imagining things. You are not wrong to be frustrated. At Panda7, we refer to this exact feeling as "Price Anxiety". Our entire mission is to eliminate it from your life forever. We believe you have a fundamental right to know exactly what you are paying for and exactly how that price is calculated.

This definitive guide is our commitment to building radical trust with you. We are going to open the notorious "black box" of auto insurance pricing. We are going to hand you the owner's manual to the industry. We will deconstruct the entire premium calculation formula for you step by step. We will show you with absolute transparency what factors are fixed, what factors are flexible, and most importantly, which powerful levers you have in your control to actively lower your price using our digital platform.

Welcome to the driver's seat.

Key Takeaways: Quebec Auto Insurance Cost Control Facts

The Formula: Your final premium is a simple formula consisting of a Base Price (statistics you cannot change) plus Your Choices (the specific levers you control online).

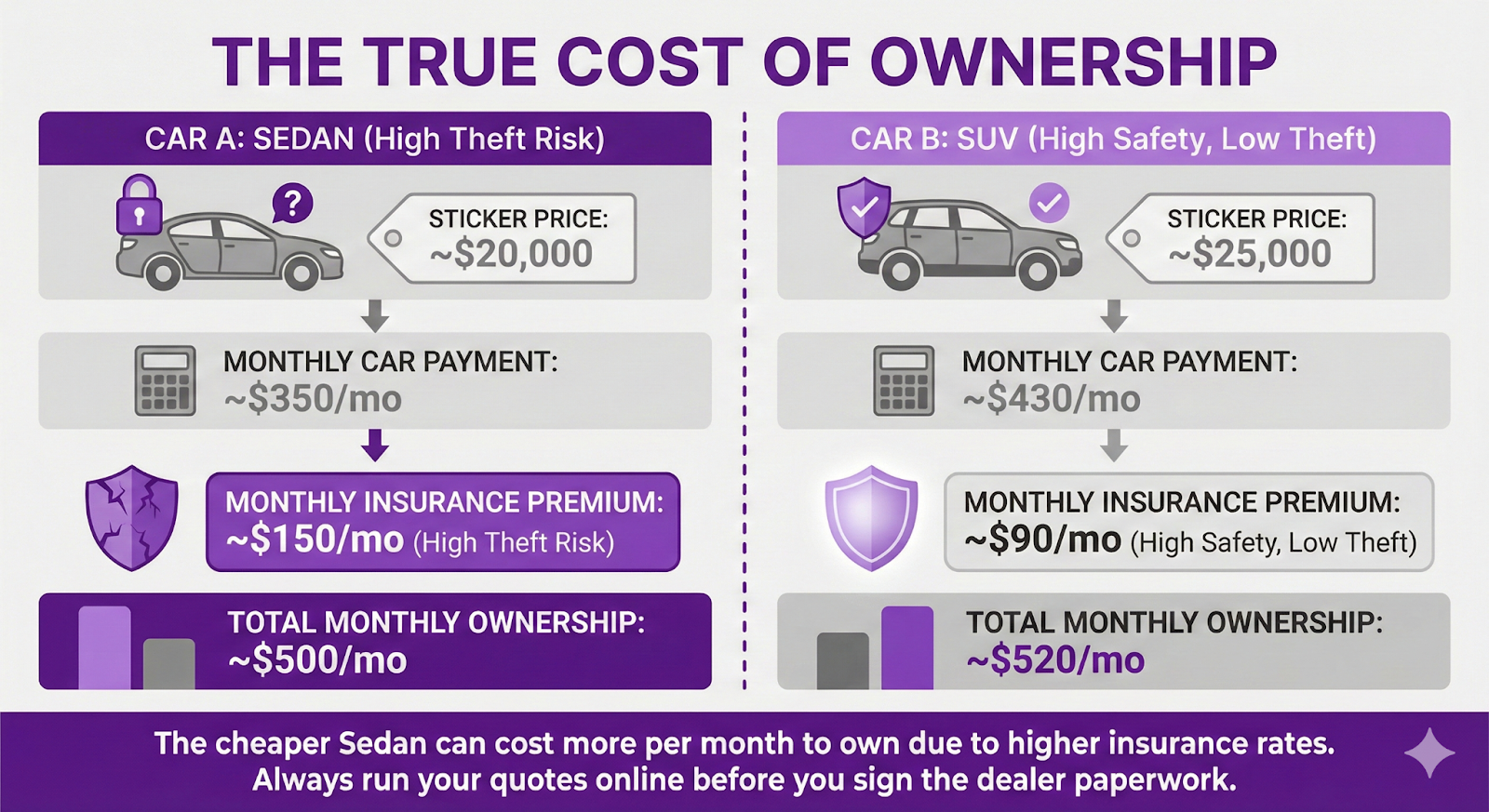

The Vehicle Impact: A car's sticker price has almost nothing to do with its insurance cost. Insurers look at repair costs and theft statistics. A luxury sedan can easily cost more to insure than a practical SUV.

The Record Reality: Insurers have wildly different rules for looking at your past tickets and claims. Our online platform scans the market to find the exact insurer who is most forgiving of your specific history.

The Financial Truth: Consenting to a soft credit check is your most powerful discount lever. It does not hurt your credit score and it unlocks massive savings.

The Golden Rule of Activation: Your auto insurance policy and your SAAQ vehicle registration must have an identically aligned effective start date to be legally valid.

The Building Blocks of Your Premium

The first step to taking control of your auto insurance cost is understanding the math behind it. Every single insurance company in Quebec calculates a base premium before they apply any of your personal choices. Think of this base premium as the raw material cost. It is a starting point based on broad market statistics that you as an individual cannot change.

This is the part of insurance that often feels unfair. But once you see the actual data behind it, you will understand exactly why shopping the market via Panda7’s smart online platform is so critical for your budget. One insurer might look at their data and decide your postal code is a massive risk, while a competitor looks at their own data and sees it as a very small risk.

Here are the main uncontrollable factors that Quebec insurers are legally permitted to consider when building your base price.

Your Postal Code and Territory Risk

Your home address tells an insurance company what kind of risk your vehicle is exposed to every single day, even when it is just parked in your driveway. Insurers use massive databases of statistics to price this risk. They look at the frequency of auto theft and the frequency of traffic collisions in your specific neighbourhood.

Industry Trap: The "Same City" Myth

The Trap: Assuming that moving to a different apartment within the exact same city will not affect your auto insurance rate.

The Truth: Quebec insurers use micro-territorial rating systems. This means neighbouring postal codes can be significantly different in cost. Moving just 2 kilometres from a dense urban core to a quieter suburb can change your monthly premium by $20 or more.

The Fix: Always use the Panda7 online quoting tool to get a new price estimate when relocating, even if you are just moving down the street.

The Real Cost of Inflation

Why is everyone's rate going up even when they have a perfect driving record? You are not imagining this trend. If your renewal price jumped this year, it is highly likely due to industry-wide factors, not because you did anything wrong.

Insurance works by pooling risk. When the cost to repair cars goes up for the entire province, the entire pool has to get bigger. High-tech repair costs are a massive factor. The advanced technology in brand new cars means a simple fender-bender that used to cost $800 now costs over $3,500 to fix due to complex sensors and backup cameras.

Auto theft frequency is another massive burden. As insurers pay out millions of dollars for stolen vehicles, they are forced to adjust the base rate upwards for high-risk models and high-risk territories. You cannot control the market's inflation, but you can control your share of it by using our platform to compare rates.

Age, Gender, and Experience

This is pure statistics. Data from insurers across Canada shows that collision frequency drops sharply after a driver reaches their first 10 years of driving experience. This is why younger, less-experienced drivers face much higher base premiums. Furthermore, while direct gender-based discrimination is prohibited as a sole factor in many regions, Quebec insurers are permitted to use statistical factors that correlate with gender for drivers under the age of 25. Data shows young males generate more at-fault claims as a group, leading to surcharges that typically disappear as they gain experience.

Your Choices: The Levers You Control

Now for the excellent news. Those fixed factors are merely the starting point. You have powerful digital tools to take control of your final price. This is where you can actively use Panda7’s online platform to lower your premium. An insurer's rating system is just a sophisticated calculator. Your job is to give that calculator the best possible numbers to work with.

You have direct control over the product you are building. The most powerful lever is choosing between one-way coverage and two-way coverage. Adjusting your deductible using our online builder can instantly save you hundreds of dollars per year. You also control whether you consent to the soft credit check, which unlocks massive discounts.

To truly master these pricing factors and see how the math works in detail, read our complete guide on How Your Quebec Auto Insurance Premium is Actually Calculated: Opening the "Black Box".

Understanding Your Vehicle's Impact on Price

This is the ultimate car buyer's nightmare. You spend weeks negotiating with a dealership. You get a fantastic deal on the sticker price of a new vehicle. You sign the financing papers, you are thrilled to drive home, and then you go online to get it insured. The premium you are quoted is $100 a month more than you budgeted for.

It feels like a setup. You are now locked into a vehicle that is going to bleed your monthly budget dry for the next 5 years.

Here is the single most important truth you need to understand about buying a car. A vehicle's sticker price has almost nothing to do with its insurance cost. Insurers do not set rates based on what the car costs you to buy. They set rates based on what that car will cost them in future claims payouts.

The CLEAR System Revealed

When you use our online platform to ask for a quote, the insurers do not guess. In Canada, most insurance companies use a standardized database called the Canadian Loss Experience Automobile Rating system. This is known as the CLEAR system.

The CLEAR database assigns a numerical rate group to every single make, model, and year of vehicle based on actual, historical claims data. It knows exactly how often a specific sedan is stolen. It knows exactly how much it costs to repair the bumper on a specific SUV. A lower CLEAR ranking means lower risk, which equals lower rates for you.

When our online platform generates your quote, it runs your vehicle's 17-digit Vehicle Identification Number through this exact system. Every character in your VIN tells a story.

SUVs Versus Sedans Versus EVs

The body type and engine of your vehicle dramatically change your rate. SUVs and minivans often have lower premiums because their weight and size provide better occupant protection, leading to fewer severe injury claims. Sports cars command the highest premiums because more horsepower leads to more frequent accidents.

Electric vehicles present a unique challenge. Do electric or hybrid cars cost more to insure than gas cars? Yes, they almost always do. While you will save a massive amount of money on gas, insurers typically charge 25% to 40% more for electric models. The high-voltage lithium-ion battery is the most expensive component in the car. If it is damaged in an accident, it can cost over $10,000 to replace. Furthermore, not every mechanic is trained to safely work on high-voltage systems. This specialized labour makes repairs much more expensive.

The Mandatory TAG Anti-Theft Requirement

This is a critical factor in Quebec and a major source of surprise bills for new car buyers. Insurers track theft data relentlessly. If you are buying a vehicle that is on their high-risk list, they will make it mandatory for you to install an approved tracking system like TAG.

This is a sudden, unbudgeted $300 to $400 installation fee just to be allowed to buy insurance. If you do not install it, insurers can hit you with a high theft surcharge ranging from $500 to $1,500 per year. Our online platform will always inform you if this requirement applies to the car you are considering before you finalize the quote.

To learn exactly how to compare vehicles and avoid these massive post-purchase surprises, read our full guide on How Your Car Really Impacts Your Insurance Price in Quebec: Your Surprise-Proof Guide.

Core Coverage Choices: One-Way Versus Two-Way

If you are confused by insurance jargon, you are not alone. The insurance industry often uses complex terms that make it incredibly hard to know if you are overpaying for protection you do not need, or worse, under-insured for a financial disaster.

The biggest choice you will make on our online platform is choosing your base coverage level. This choice is often made for you by one simple, golden rule. It all comes down to who owns the vehicle.

If your vehicle is financed or leased, you are legally required to have full two-way coverage. The lender or leasing company has a financial interest in the car, and this coverage protects their asset until the loan is fully paid. If your vehicle is paid off, you have the total freedom to choose one-way coverage to save money.

Deep Dive: One-Way Coverage

One-way coverage is the absolute cheapest legal minimum auto insurance you can buy in Quebec. Its official name is Civil Liability coverage.

This policy covers property damage you cause to others. It also covers damage to your own car, but only if you are not at fault in a collision that occurred in Quebec. It also covers your liability for bodily injuries caused to others in accidents outside of Quebec.

However, one-way coverage does not cover damage to your car from an at-fault accident. It also provides absolutely zero coverage for theft, vandalism, fire, glass damage, or hitting an animal. This is a popular and highly recommended budget-friendly choice for drivers of older, fully-paid-off cars who are comfortable paying for their own repairs in exchange for the absolute lowest possible premium.

Liability Limits and US Coverage

When you purchase Civil Liability coverage, you must select a financial limit. The provincial minimum in Quebec is $50,000. However, this amount is dangerously low for modern driving. We strongly recommend selecting a limit of $1 million or $2 million to fully protect your assets in the event of a severe lawsuit.

If you ever drive your vehicle into the United States, a $2 million limit is highly recommended. Your Quebec policy automatically extends your coverage to the United States and the rest of Canada. However, American medical and legal costs can easily bankrupt a driver who only carries the provincial minimum. Using our online tools to increase your liability limit is incredibly inexpensive and provides massive peace of mind.

Deep Dive: Two-Way Coverage

Two-way is not an official policy name. It is a common term that simply means you have one-way Civil Liability plus two essential protections for your own vehicle.

The first is Collision Coverage. This covers your car if you are at fault in an accident, such as hitting another car or sliding into a pole. The second is Comprehensive Coverage. This covers your car for almost everything else, including theft, vandalism, fire, windshield glass damage, and hitting an animal. This is the peace of mind package.

Industry Trap: Two-Way is NOT New-For-Old

The Trap: Believing that having full two-way coverage on a brand-new car means the insurer will buy you a brand-new car if yours is totaled in a crash.

The Truth: Standard two-way insurance only pays for the actual cash value of your car at the exact moment of the accident. A car depreciates the second you drive it off the dealership lot.

The Fix: To get a brand-new replacement car, you must purchase a distinct, optional add-on called Replacement Cost (Valeur à Neuf). You can easily add this using our online quoting platform.

Stop Overpaying for Optional Extras

You can take massive control of your budget by dropping optional add-ons that no longer serve you. Replacement Cost is crucial for a brand new vehicle, but it becomes an absolute waste of money as the car ages.

Another highly debated add-on is the Courtesy Car endorsement, officially known as Rental Car Coverage (Endorsement 20). This pays for a temporary rental car while your vehicle is in the shop after a covered claim. Declining this can save you up to $8 a month. Roadside Assistance (Endorsement 33) costs up to $80 a year. If you already have roadside assistance through your credit card, declining it is an easy way to avoid paying twice for the exact same service.

To master your coverage choices and learn exactly how to balance your deductibles, read our complete guide on One-Way vs. Two-Way Insurance in Quebec: Your Plain-Speak Guide.

How Your Personal Record Affects Your Rate

It is one of the most frustrating feelings in the world. You shop for a new quote online, and the price is shockingly high. You immediately think of that one speeding ticket from two years ago or that minor fender-bender you could not avoid. You feel penalized, stuck, and powerless.

If you have been told your past tickets or claims will automatically raise your rate for a fixed number of years everywhere you go, you have only been given half the truth.

Your past is fixed. The price you pay for it is not. The single biggest secret in the insurance industry is that different insurers in Quebec penalize the exact same incident in wildly different ways.

The Two-File Secret

To feel empowered, you first need to understand what insurers actually see when you request a quote. In Quebec, your driver profile is split into two completely separate files. Insurers pull both of them.

First is your SAAQ Driving Record. This tracks your license status and convictions for traffic violations. Second is your GAA Claims History file. This tracks every single insurance claim filed in the past 6 years.

Here is the key takeaway that is your biggest strategic advantage. Insurers and brokers cannot see your SAAQ demerit points. They see the conviction (the ticket itself), but not the points.

The Insurer Lottery

Not all insurers are the same. They have different memories, different corporate rules, and different appetites for financial risk. This variability creates a lottery for shoppers who do not use an online comparison platform. One insurer might see a 4-year-old claim and charge you a hefty premium. A competitor might see the exact same claim and charge you nothing extra.

Some insurers penalize an at-fault claim for the full six years it remains on your central file. Others only look back 3 years. If you have a claim from 4 years ago, a strict insurer will charge you a massive penalty. A forgiving insurer will view you as a driver with a perfectly clean record.

This is exactly how Panda7 empowers you. Our smart online platform knows exactly which insurer is which. We do not guess. Our platform matches your specific history to the most forgiving insurer in the market, instantly wiping unnecessary surcharges off of your monthly bill.

The Power of Accident Forgiveness

You can proactively protect your driving record from future mistakes by adding an Accident Forgiveness endorsement to your policy.

If you purchase this optional coverage before a collision occurs, the insurance company agrees to ignore your very first at-fault accident when calculating your future premium. This “Good Record Protection” ensures that a mistake doesn't immediately raise your rate at renewal.

To learn exactly how to navigate past tickets, claims, and your central file, read our complete guide on How Past Tickets & Claims Really Impact Your Quebec Auto Insurance Price.

How Your Credit and Financial History Impact Price

Let us talk about the single most uncomfortable moment in getting auto insurance. It is when the online form asks for your permission to check your credit. For most people, this feels highly intrusive. Your mind immediately goes to the common anxieties. Will this hurt my credit score? Are they using this to add hidden fees to my premium?

Your financial history is not a moral judgment. It is simply a set of highly effective price levers. Some of these levers are among the most powerful tools you have to lower your premium.

The Soft Credit Check Lever

We must bust the biggest myth in the industry right now. Checking your credit for an auto insurance quote in Quebec will have absolutely zero impact on your credit score.

Consenting to the check is a price lever that is entirely in your control. It is how you unlock the good credit discount that most insurers offer. This discount can lower your premium significantly. Refusing the check does not hide your history. It simply forces the insurance company to assume you are a higher risk, which guarantees you will forfeit a massive discount.

When an insurer checks your credit via our online platform, it is a soft pull. It is not a hard pull like a loan application.. You can get 10 quotes from our platform today, and your score will not drop a single point.

Insurers do not use your standard bank credit score. They use an insurance score that predicts the likelihood you will file claims. This score weighs your payment history heavily, followed by outstanding debt, the length of your credit history, and your pursuit of new credit. They are legally forbidden from seeing or using factors like your income or race. This system is designed solely to reward consistent financial behavior.

Bundling and Flexibility

One of the most powerful levers for immediate financial savings is bundling. By insuring your vehicle and your home or apartment with the exact same company using our digital tools, you unlock a multi-line discount that can instantly lower your total premium by 10% to 15%.

Furthermore, your policy offers extreme flexibility. You are never locked into your choices. You can log into our online platform mid-year to adjust your deductibles or change your coverage limits to match your changing budget. You have total control.

The Three-Year Reset for Cancellations

A past non-payment cancellation does put you in a higher-risk category. This limits your options to specialized insurers and means a higher starting premium. However, it is absolutely not a permanent penalty.

When a cancellation happens, a notation is added to your insurance history file. This mark remains visible for approximately three years. The consequences are real, but you can stop the spiral. After three years of clean insurance history with a high-risk provider, standard insurers will become willing to offer you excellent coverage again, and your rates will drop significantly.

Ratable Lapses Versus Innocent Gaps

Will a gap in your insurance history ruin your chances of getting a low rate? Not necessarily. It depends entirely on the reason for the gap.

If you did not own a car because you sold your old one and haven't bought a new one yet, insurers do not penalize you. You are still viewed as having a continuous history. However, if you owned a vehicle but let the insurance expire while it sat in your driveway, this is considered a ratable lapse. This is viewed as high-risk behavior and will lead to a higher premium for a few years.

To fully understand your financial profile and how to leverage your credit score for maximum savings, read our guide on Your Financial Profile: How to Take Control of Your Auto Insurance Rate in Quebec.

Navigating the Policy Activation Process

This is the part of buying auto insurance that feels deliberately designed to be confusing. It is not just about finding a great price online. It is about navigating a maze of logistical rules and SAAQ appointments. You are left wondering if you are actually legally insured to drive your new car off the dealership lot.

That anxiety is valid. We are going to pull back the curtain on the entire activation process so you can finalize your policy online with absolute confidence.

The Golden Rule of Activation

Here is the single most important rule in the entire activation process in Quebec. Your auto insurance policy and your SAAQ vehicle registration must have an identically aligned effective start date.

This is a strict legal requirement. When you go to an SAAQ service outlet to register your vehicle, you are legally required to have a valid private insurance policy in place for that exact day. You cannot register a car today with an insurance policy that starts tomorrow. The policy must be live at the moment of registration.

Our online platform eliminates this risk entirely. When you checkout, you set your policy start date to precisely match your SAAQ registration date, ensuring you are legally covered with zero gaps.

The Five-Step Online Path

The activation process is incredibly simple when you use modern digital tools.

- Step one is getting your quote. You provide your details and consent for a soft credit check on our platform.

- Step two is finalizing your details through our secure online checkout.

- Step three is the final verification. The insurer runs your file through their central system one final time to verify your official driving record against the information you provided online.

- Step four is the policy issuance. Once verified, the policy is officially bound. Your premium is now locked in for the full 12-month term.

- Step five is immediate active coverage. We instantly email you your digital proof of insurance. You can confidently show this PDF document on your smartphone to the dealership or police officer as legally valid proof of coverage.

To learn exactly how to handle out-of-province licenses, grace periods, and instant digital documents, read our step-by-step guide on How to Activate Your Auto Insurance in Quebec: A Step-by-Step Guide.

Get the Playbook That Beats the System.

You now understand the math, the rules, and the exact levers you control. Take the next step to lower your premium. Get our complete, expert email playbook that gives you the exact strategies to beat the “black box” and lock in the best rate—sent right to your inbox.

The Ultimate Auto Insurance FAQ

You have questions. We have plain-speak answers. We have compiled the most critical questions from our entire Awareness Stage research to ensure you have every piece of knowledge necessary to control your costs.

General Pricing and Formulas

Once I get a final quote online, can that price still change?

Yes, but only if your official record differs from what you typed into the online form. When you finalize your purchase, the insurer’s central system recalculates the premium using your official data. If you forgot about a recent speeding ticket, the system automatically adjusts the rate. Our online platform ensures you see the most accurate price possible before you finalize your payment.

Are taxes included in the auto insurance quotes I see online?

The initial estimate rates you see might not include tax, but the final bindable checkout price always will. Every auto insurance policy sold in Quebec is subject to a nine percent provincial sales tax. This tax is transparently added to your premium before you finalize your purchase. Please note that effective January first of 2027, this tax will be harmonized with the QST, increasing to 9.975 percent.

How do insurers get data on vehicles to set their rates?

Quebec insurers contribute anonymized claims and risk data to central industry databases. This collective data is analyzed annually to update the risk profiles for every vehicle make and model across every geographical region.

What small changes can move my premium up or down between quotes?

Moving your policy start date or rounding your annual mileage estimate up or down on our platform can easily shift the insurer’s rating algorithm and change your premium.

Driving Records and Claims History

What is the difference between my SAAQ driving record and my central claims history?

These are two completely separate files. Your SAAQ driving record tracks your licensing status and convictions for traffic violations like speeding tickets. Your central claims history tracks every insurance claim filed in the past six years, showing fault percentages and payouts. Insurers cross-reference both files.

If I have multiple old claims, will every insurer count them the same way against me?

No, and this is the most important reason to use our online comparison platform. While the central file tracks all claims for six years, individual insurers have complete discretion in how far back they look. One insurer might surcharge you heavily for a 5-year-old claim, while a competitor with a 3-year rating window ignores it entirely.

Does the dollar amount of my past claim affect how much my premium increases?

For the vast majority of insurers, it is the mere fact that you made an at-fault claim that triggers the surcharge. It is not the payout size. Whether your repair was minor or severe, you are typically flagged identically as having one at-fault claim on record.

How long do I have to wait after a ticket before it stops affecting my premium?

For tickets, most insurers surcharge you at each renewal for the 3 full years the ticket remains on your SAAQ record. Please note that while demerit points expire from your license after only 2 years, insurers continue to rate the conviction itself for the full 3rd year.

If I had an accident in a rental car, will it appear on my personal insurance record?

Yes. In Quebec, the central claims file tracks you as a driver, not just as a vehicle owner. Any accident where you were the driver is added to your personal claims history statement, regardless of whose vehicle was involved.

I have a perfect record except for one not-at-fault accident. Why is my premium going up?

This is a highly frustrating reality. Even when you are proven completely innocent in a collision, that claim is still recorded in the central file. Some insurers flag any claim history as a statistical indicator of future risk. Our online platform knows which Quebec insurers do not penalize innocent drivers and will steer you toward them.

If I pay for a minor accident out-of-pocket, do I still have to report it to my insurer?

Yes, you are legally required to. Quebec insurance regulations require you to report any accident to your insurer, even if you do not intend to file a financial claim. This protects you in case the other party decides to file a lawsuit later.

Financial Profiles and Credit Checks

Will checking my credit for a quote online hurt my credit score?

No. It will have absolutely zero impact. Insurers use a soft pull inquiry. This type of check is only visible to you and other insurance companies. It does not lower your credit score. You can compare ten different quotes on our platform today, and your score will remain completely untouched.

How much can my credit score actually save me in Quebec?

The impact is massive. According to official data from the Autorité des marchés financiers, credit information can influence your premium by anywhere from a 30% discount to a 15% surcharge. Consenting to the check on our platform is the fastest way to lower your rate.

What exactly is an insurance score?

Insurers do not use your standard bank credit score. They use an insurance score that predicts the likelihood you will file claims. This score weighs your payment history heavily, followed by outstanding debt and the length of your credit history. They are legally forbidden from seeing your income or race.

I had an auto insurance policy cancelled for non-payment. Am I stuck with high rates forever?

Not at all. A non-payment cancellation puts you in a higher-risk category for about three years. Standard insurers will likely decline your application during this time. However, our online platform connects you with specialty markets designed for these profiles. After three years of clean payment history, the penalty fades and you can return to standard rates.

Does being a secondary driver on my parent's policy count as my own insurance history?

Unfortunately, no. Insurers only count experience when you were the primary policyholder or the principal driver assigned to a vehicle. You will typically be rated as a newly insured driver when you get your own first policy.

Does a discharged bankruptcy stop me from getting insured?

No. Once your bankruptcy is officially discharged, most standard insurers treat it as a closed matter. It normally has no impact on your eligibility or price, allowing you to access standard rates immediately.

Coverage Choices and Trade-Offs

What happens if I change from two-way to one-way mid-policy? Are there hidden penalties?

No, there are no hidden penalties. You can typically use our online platform to make this change at any time, provided your car is fully paid off. Your annual premium is simply recalculated for the remaining days in your term, and your monthly payments will drop accordingly.

How do claims work if both drivers have one-way liability coverage?

Under Quebec direct compensation rules, if the other driver is fully at fault, your own insurer covers your repairs even if you only purchased one-way coverage for yourself. The insurance level chosen by the other driver does not affect your payout at all.

If my car is financed, does the lender require a special endorsement?

Yes. When a vehicle is financed, the lender requires a standard Loss Payee endorsement. A leased vehicle requires a slightly different endorsement. These simple additions list the finance company on your policy so they are notified of any changes and ensure they are paid first in the event of a total loss.

What does the mandatory private auto insurance policy in Quebec actually cover?

The mandatory Civil Liability policy covers property damage you cause to others. This applies when you drive your own car or a borrowed one. It also covers your liability for bodily injuries caused to others in accidents that occur outside of the province of Quebec.

Vehicle Impacts and Risk Ratings

What is the single best thing I can do to avoid a surprise insurance hike?

Get an insurance quote online before you buy the car. The sticker price of a car is not an indicator of its insurance cost. Enter the seventeen-digit VIN into the Panda7 smart platform before you sign the dealership papers to guarantee you know your true monthly cost of ownership.

Will my premium be the same if I switch to a different vehicle of the same age and price?

Not necessarily. Each specific vehicle model has its own distinct risk profile based on historical claims data. One older sedan might have a massive theft rate in your city, while another older sedan has incredibly low repair costs.

Why do luxury cars and sports cars cost so much more to insure?

They cost more for three main reasons. First, specialized imported parts and advanced sensors drive repair bills dramatically higher. Second, more expensive engines correlate with higher accident severity. Third, statistical data shows that drivers of high-performance vehicles are more likely to engage in risky driving behaviors.

Do trim levels and optional equipment features affect my insurance premium?

Yes, they can meaningfully affect your premium. Higher trim levels of the exact same model cost more to insure because they include more expensive features like upgraded engines, leather seats, and advanced technology.

Does buying a used car versus a new car affect my insurance costs?

Yes, but the relationship requires context. Newer vehicles often cost more to insure because they have a higher market replacement value and more expensive technology to repair. Used vehicles are cheaper to replace, but if they lack modern safety features or have notoriously high theft rates, their insurance can still be shockingly high.

What happens to my insurance rate if I lease a vehicle versus buying it?

Leasing has significant insurance implications. Leased vehicles always require mandatory full two-way coverage because the leasing company owns the asset and must protect it. This means leased vehicles typically have higher insurance costs simply because you cannot choose a cheaper, liability-only policy to save money.

Can an auto insurer force me to install an anti-theft device like a TAG system?

Yes. While a TAG system is often an optional discount, insurers will make it completely mandatory for specific models that have a high rate of theft in Quebec. If you are buying a vehicle on this high-risk list, the insurer will require you to have an approved tracking system installed at your own expense before they will agree to insure it against theft.

The Activation and Synchronization Process

Do I have to insure my car the exact same day it is registered in my name?

Yes. This is the most important legal rule. Quebec law requires you to have active insurance from the exact moment the vehicle is registered in your name at the SAAQ. You cannot legally complete the registration process without having a valid private insurance policy already active for that specific calendar day.

Does my current policy automatically cover a newly purchased vehicle for a short time?

Yes, but in very specific cases. If your new vehicle completely replaces a car that is currently insured on your policy, most Quebec auto policies extend your existing coverage to the new vehicle for a short grace period of about 14 days. This automatic coverage does not apply if you are adding an additional second car to your household. You must insure an additional car before you drive it.

I am moving to Quebec from another province. How do I handle activation?

You should use our online platform to get an insurance quote in advance using your out-of-province documents. However, your actual Quebec auto insurance policy cannot activate until your vehicle is officially registered and plated with the SAAQ.

Can I insure a car that is registered to my spouse if I am the primary policyholder?

Technically, yes. You can insure a vehicle registered to your spouse if you explicitly declare the ownership difference to the insurer on our platform. While legal, some insurers prefer the registered owner to be the main policyholder to avoid massive complications with claims payouts or financing agreements.

Continue Your Research

This page serves as your master blueprint for auto insurance cost control. To master the specifics of each topic, please continue exploring our deep-dive guides.

- To learn about the exact math behind your base price, read our guide onHow Your Quebec Auto Insurance Premium is Actually Calculated: Opening the "Black Box".

- To understand how the SAAQ and GAA files operate, read our guide onHow Past Tickets & Claims Really Impact Your Quebec Auto Insurance Price.

- To master the credit check and non-payment rules, read our guide on Your Financial Profile: How to Take Control of Your Auto Insurance Rate in Quebec.

- To fully unpack liability versus full coverage, read our guide on One-Way vs. Two-Way Insurance in Quebec: Your Plain-Speak Guide.

- To see exactly how the CLEAR system rates your car, read our guide on How Your Car Really Impacts Your Insurance Price in Quebec: Your Surprise-Proof Guide.

- To ensure a flawless SAAQ registration experience, read our guide on How to Activate Your Auto Insurance in Quebec: A Step-by-Step Guide.

Ready to take the next step and apply these strategies to a live comparison? Move forward to our consideration guide to learn actionable shopping tactics: Provide Actionable Savings Strategies.

Data Sources & Methodology: Panda7 is committed to radical transparency. The statistical and regulatory information on this page is sourced directly from:

- Source 1: Autorité des marchés financiers (AMF). Regulatory framework for Quebec insurance brokers and credit data reports.

- Source 2: Groupement des assureurs automobiles (GAA). Territory risk and Fichier central des sinistres automobiles (FCSA) claims data.

- Source 3: Société de l'assurance automobile du Quebec (SAAQ). Public bodily injury plan and driver licensing data.

- Source 4: Insurance Bureau of Canada (IBC). The provider of the Canadian Loss Experience Automobile Rating (CLEAR) system data.

- Source 5: Insurance Institute for Highway Safety (IIHS). Independent vehicle safety rating statistics.