TAG Tracking Systems and Anti-Theft Requirements for Auto Insurance in Quebec

Buying a new car should be a moment of celebration, not administrative stress. Yet, for many Québec drivers, the excitement of the dealership fades the moment the finance manager hands over the insurance requirements checklist. Suddenly, you are facing terms like "Loss Payee," "Endorsement 23," and "Mandatory TAG Installation."

It is natural to feel skeptical. When a lender or insurer demands extra clauses or expensive tracking devices, it often feels like just another hidden fee designed to inflate your monthly payments. You might worry that missing a single detail could delay your delivery or, worse, void your coverage later.

Here is the reality:

These requirements are not traps.

They are the standard safeguards of the Québec auto market, and they are entirely manageable.

At Panda7, we believe you should never be intimidated by fine print. The purpose of this guide is to translate these banking and insurance mandates into plain language.

We will explain exactly why lenders require specific protections and how to satisfy them without overpaying. We will break down the math of anti-theft systems to show you when they are a smart investment versus a sunk cost. And we will help you navigate the "Small Lender" hurdles that trip up so many financed drivers.

Your goal is to drive away with confidence. Our job is to handle the paperwork that gets you there.

Key Takeaways: Lender & Anti-Theft Facts

The "Two-Way" Mandate: If you finance or lease a car, you must have full coverage (Collision and Comprehensive). The bank owns the asset and requires you to insure it against physical damage.

The "Loss Payee" Clause: Your lender must be listed on your policy. This ensures they receive payment first if the car is a total loss. It costs nothing but is mandatory to take possession of the vehicle.

The "Small Lender" Check: Not all insurers accept loans from small private financing companies. Use the Panda7 quote tool to filter for carriers that accept your specific lender.

The TAG Math: An anti-theft tracking system costs roughly $400 upfront but can save you $50-$100 annually in premiums. For high-risk vehicles, it is often a mandatory condition for theft coverage.

The 7-Day Timer: If a TAG system is required, you typically have a 7-day grace period to install it. Missing this window can trigger a significant price increase or a removal of theft coverage.

Phase 1: Navigating Lender Requirements (The Bank's Rules)

When you finance a vehicle, you enter into a partnership with your lender. Whether it is a major bank or a dealership financing arm, the lender retains a financial interest in the car until the final payment is made. To protect that asset, they impose strict insurance conditions. These are not suggestions, they are contractual obligations. Failing to meet them can put your loan in default.

Here is how to ensure your policy satisfies these conditions automatically.

The "Two-Way" Coverage Requirement

The most fundamental rule of financing is that you cannot carry "One-Way" (Civil Liability only) coverage on a vehicle you do not fully own.

- The Logic: If you are in an at-fault accident without Collision coverage, the insurance company pays nothing for your vehicle repairs. You would be left with a wrecked car but still owe the full balance of the loan.

- The Consequence: Most drivers in this situation stop making loan payments because they have no car to drive. This is the specific risk lenders mandate against.

To prevent this, lenders require Chapter B coverage (Damage to Insured Vehicle), commonly known as "Two-Way" coverage. This includes:

- Collision: Covers repairs if you hit another vehicle or object.

- Comprehensive: Covers non-collision events like theft, fire, or vandalism.

- Maximum Deductibles: Lenders typically cap your deductible at $1,000 to ensure you can afford the out-of-pocket cost to repair the vehicle.

The Panda7 Fix: Panda7 makes compliance simple. Our platform is designed to help you identify and select the mandatory coverage levels required by lenders, protecting you from buying a policy that violates your loan agreement.

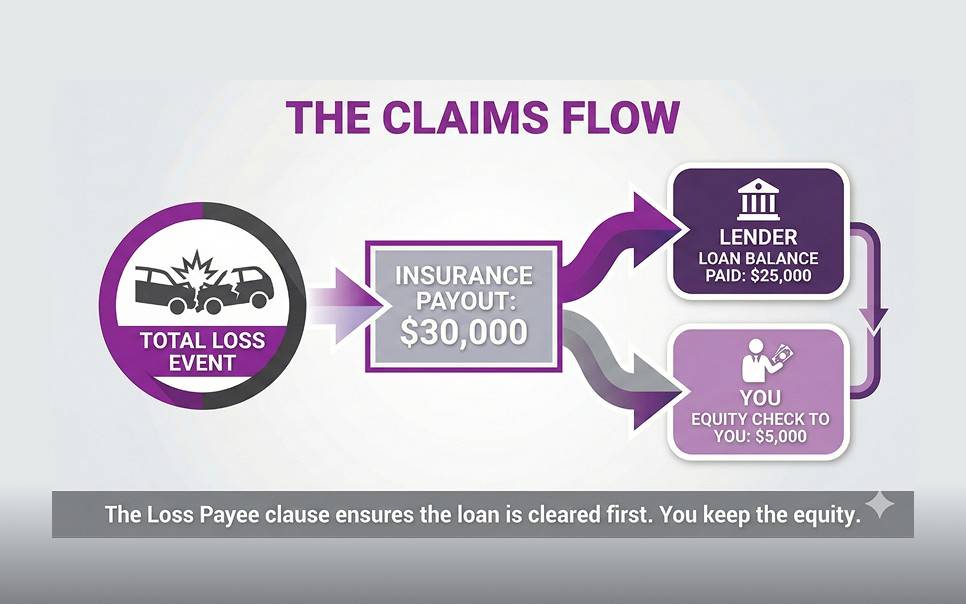

The "Loss Payee" Designation (Endorsement 23)

This is often the final hurdle at the dealership. The finance manager will verify that the bank is listed as the "Loss Payee" on your proof of insurance.

- What it means: This endorsement legally establishes that in the event of a "Total Loss" (where the car is written off), the insurance payout is issued jointly to you and the lender.

- How it works: The insurer pays the lender the outstanding loan balance first. Any remaining equity is then paid to you.

- The Cost: There is no charge for this endorsement. It is a standard administrative notation.

Phase 2: The "Small Lender" Hurdle

For drivers who finance through "Second Chance Credit" or smaller private lenders, there is a specific anxiety: Will my choice of lender make me uninsurable?

The Reality: Using a non-traditional lender does not make you uninsurable, but it does narrow your options.

Direct insurers often have rigid "Approved Lender Lists." While they universally accept major banks (like RBC or Desjardins), they may automatically decline applications linked to smaller, high-interest financing companies. This rejection is rarely explained; you are simply told you do not meet underwriting criteria.

How We Handle It: Panda7 operates differently. We understand the underwriting guidelines of over 10 insurers, including those like Pafco that specialize in accommodating alternative financing arrangements.

At Panda7, we don't just guess. We work with carriers that specialize in different financing situations. By comparing multiple insurers, we help you find one that accepts your specific lender, turning a potential decline into a competitive quote.

Phase 3: The Anti-Theft Mandate (TAG Tracking)

Auto theft is a significant issue in Québec, particularly for high-demand vehicles like SUVs, pickups, and luxury sedans. To mitigate this risk, insurers have moved beyond asking for anti-theft precautions—they now demand them.

This often leads to the frustration of being asked to pay $400 for a device on top of your insurance premiums. The key is to reframe this expense: It is not a tax; it is an investment with a calculated return.

The TAG System Explained

TAG is a robust, covert tracking system. Unlike a standard car alarm, technicians install multiple wireless transponders hidden throughout your vehicle. These devices are difficult to jam and allow the TAG team to track stolen vehicles anywhere in North America with a near 100% recovery rate.

The Mandate: If you drive a high-theft model—such as a Honda CR-V, Toyota RAV4, or Ford F-150—most insurers will refuse to offer theft coverage unless a TAG system is installed.

The Cost-Benefit Analysis

Let's break down the financial impact.

- The Cost: A standard TAG installation is a one-time fee of roughly $300-$400. Crucially, there is usually no monthly subscription fee.

- The Savings: Insurers provide an "Anti-Theft Discount," typically reducing your annual premium by $50-$100.

- The Surcharge Avoidance: This is the most critical factor. If you decline to install a TAG system (assuming the insurer allows it), you may face a "High Theft Surcharge" of $500 to $1,500 per year.

The Math: Spending $400 once to avoid a recurring $500 annual surcharge is a clear financial win. In this scenario, the device pays for itself in less than a year.

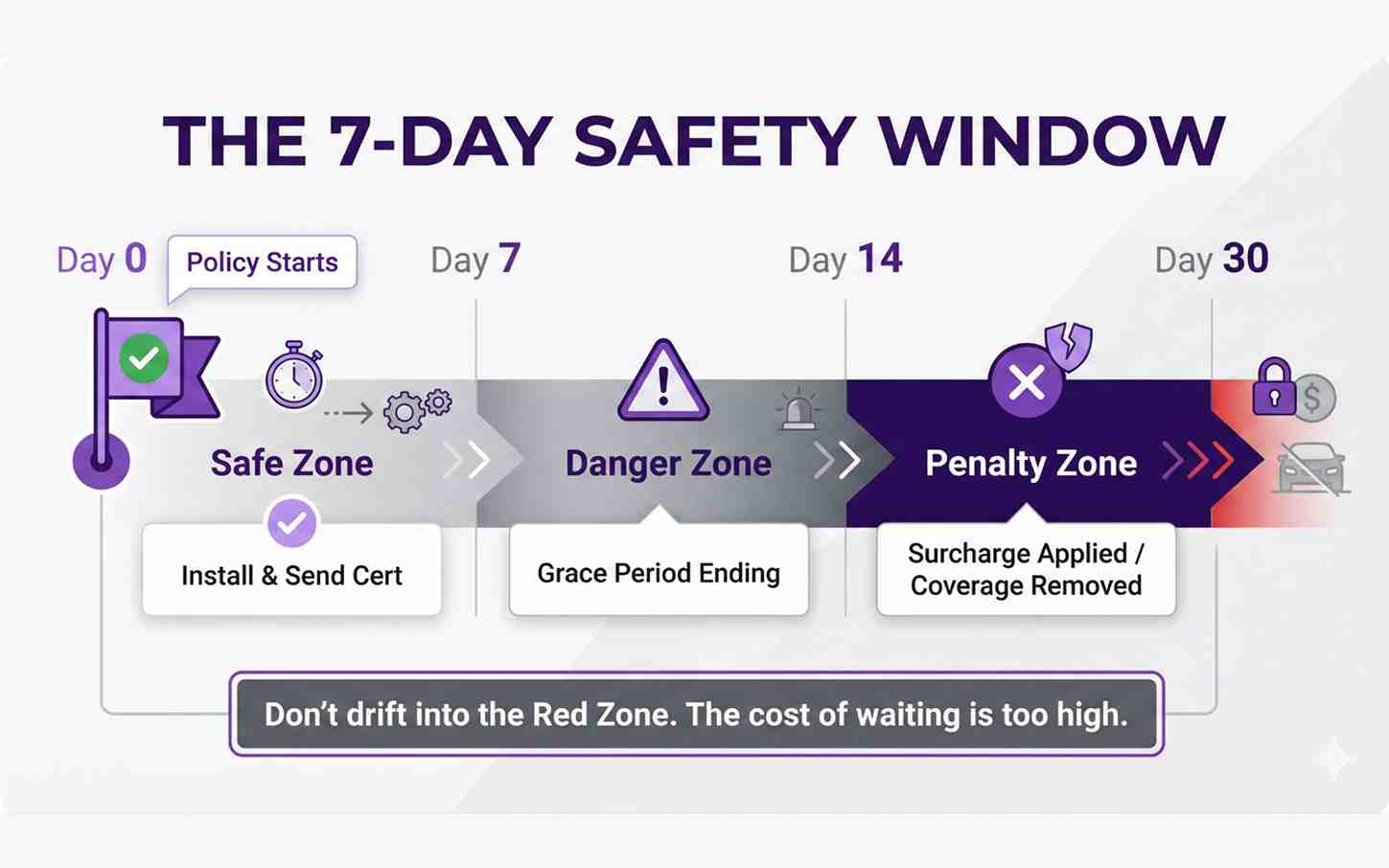

Phase 4: The Installation Timeline (The 7-Day Rule)

Timing is critical. A common mistake is purchasing a policy and then delaying the TAG installation.

The Consequence: Insurers enforce a strict grace period, typically roughly one week from the policy start date. If the installation certificate is not submitted by the deadline, one of two things happens:

- The Price Hike: The insurer removes the discount and applies the High Theft Surcharge retroactively. Your monthly payment increases immediately.

- The Theft Exclusion: The insurer removes theft coverage entirely. If your vehicle is stolen after the grace period, you receive $0.

The Strategy: Arrange for installation before or immediately after taking possession of the car. Many dealerships offer on-site installation. Once installed, text or email the certificate to your Panda7 broker immediately to lock in your discounted rate permanently.

Phase 5: The "Used Car" Transfer Trick

There is a simple way to save $400 on installation if you are buying a used vehicle: Check if it already has a TAG system.

- The Mistake: Buying a new system because you assume the car is unprotected.

- The Fix: Inspect the driver's side window for the TAG logo or ask the seller explicitly.

The Transfer: If a system is present, you do not need to buy new hardware. You simply pay a small "Transfer Fee" (typically $50-$100) to register the existing units in your name.

The Process:

- Contact TAG with the vehicle's VIN.

- Confirm the existing units are active.

- Pay the transfer fee online.

- Download your new "Installation Certificate."

- Submit the certificate to Panda7.

By verifying first, you save the cost of a new installation while securing the full insurance discount.

Phase 6: The "Hidden" Protections Your Lender Won't Mention

Lenders prioritize their own financial recovery, which is why they mandate Collision Coverage. However, standard financed policies often leave you financially exposed in other ways. We call these "Financial Stability Endorsements."

Replacement Cost (Endorsement 43) vs. Gap Insurance

New vehicles depreciate the moment they leave the lot. If you suffer a total loss a year later, the market value of the car may be less than the remaining loan balance.

The Solution: You have two primary options to bridge this gap.

- Gap Insurance: Typically sold by dealerships, this covers only the difference between the car's depreciated value and your loan balance. It settles the debt but leaves you with no vehicle.

- Replacement Cost (Endorsement 43): Sold by Panda7, this option is superior. It covers the cost of purchasing a brand new vehicle of the same make and model, rather than just paying off the loan. However please note that this specific endorsement generally does not cover negative equity (debt rolled over from a previous vehicle). If you have rolled-over debt, verify if your Gap policy specifically covers this “balloon” amount, as not all do.

Strategic Advice: Before purchasing dealer Gap Insurance, request a quote for Endorsement 43. It is often more affordable and provides significantly better protection, replacing your car rather than just your debt.

Loss of Use (Endorsement 20/20a)

This is a frequently overlooked protection. If your vehicle is in the shop for weeks following an accident, your loan payments do not stop.

- The Problem: You must continue paying your loan plus roughly $50/day for a rental car out of pocket.

- The Fix: Endorsement 20 covers the cost of a rental vehicle while yours is being repaired.

- The Logic: For an annual cost of approximately $60, this endorsement protects your cash flow and ensures you can continue getting to work to earn the money to pay that loan.

Bundling: The Ultimate Offset Strategy

The most effective way to neutralize the cost of a mandatory TAG system is to bundle your insurance.

Combining Tenant or Home insurance with your Auto policy typically triggers a 10% to 15% Multi-Line Discount. For a standard auto premium of $1,200/year, a 15% saving equals $180. That savings effectively covers half the TAG installation cost in year one and becomes pure profit in subsequent years. You can quote both lines simultaneously in the Panda7 tool.

Phase 7: Québec Specifics (Tax & Registration)

Québec's insurance landscape has unique costs that must be factored into your budget.

The 9% Sales Tax

In Québec, all auto insurance premiums are subject to a 9% provincial sales tax, which increases to 9.975% on Jan 1 2027.

- The Shock: receiving a bill that is higher than the quoted base premium.

- The Reality: This is a mandatory government tax collected by all insurers, not a hidden broker fee. Always add 9% to your calculated budget to avoid surprises.

The SAAQ Registration Sync

Your insurance policy must match your SAAQ registration details exactly. Furthermore, you typically need valid proof of insurance before the SAAQ will issue your license plate.

The Sequence:

- Obtain the VIN from the seller.

- Secure your Panda7 quote and bind the policy.

- Receive your digital proof of insurance via email.

- Present the proof at the SAAQ counter.

- Receive your license plate.

Phase 8: Step-by-Step Guide to Compliance

Follow this checklist to move from "Quote" to "Keys in Hand" seamlessly.

Step 1: Gather Lender Details Request the exact legal name and address of your financial institution from the finance manager. Ask if they require a specific "Loss Payee" address for insurance correspondence.

Step 2: Run the Quote with "Financed" Selected Use the Panda7 quote tool. Be sure to indicate that your vehicle is 'Financed' or 'Leased' so the necessary coverage options are included. Providing the lender's name accurately helps ensure the right endorsements are applied.

Step 3: Check for Anti-Theft Mandates Review the quote details carefully. If "Anti-Theft Device Required" is listed, call a local shop immediately to check pricing and availability.

Step 4: Bind the Policy Lock in your price and complete the purchase online.

Step 5: Distribute the Proof Forward the proof of insurance email immediately to your dealership's finance manager. This document is the "ticket" required to release the vehicle.

Step 6: The Post-Purchase Follow-Up If a TAG was required, ensure it is installed within the first week. Text a photo of the certificate to your Panda7 broker to verify the discount is applied.

See Your True Cost & Lender Options

Don't guess about surcharges. See which insurers accept your lender, calculate your exact anti-theft savings, and lock in your price with zero surprises.

Get Your QuoteExpert Answers to Your Requirement Questions

What is the difference between a "Loss Payee" and a "Lender's Loss Payable" endorsement?

Both protect the lender but offer different levels of security. A Loss Payee (Endorsement 23) simply lists the lender on the total loss check. A Lender's Loss Payable clause is stricter, guaranteeing the lender is paid even if you violate policy terms (such as through fraud). Most standard Québec car loans only require the standard Loss Payee clause, which is free.

If my car is financed by a small credit union will insurers decline me?

It is possible. Major "direct" insurers often decline loans from non-approved lenders. Panda7 works with over 10 carriers, including specialty insurers like Pafco and Economical, allowing us to find a carrier that accepts your specific private lender and turning a potential "No" into a "Yes."

What is the break-even point for a TAG anti-theft device?

For optional installations, the break-even point is typically 3 to 5 years. If the device is mandatory, the break-even is immediate. The "surcharge" for not having it on a high-risk car can be $500/year; avoiding that penalty pays for the $400 device in the first year alone.

I missed the 7-day window to install my TAG. Is my policy cancelled?

Not immediately, but it becomes expensive. Most insurers will remove the theft discount and apply the surcharge retroactively to day one, causing your next payment to spike. Send the certificate immediately to reverse future surcharges, although you may still owe the higher rate for the weeks you missed.

Can I transfer an existing TAG system from a used car to my name?

Yes, and you must. The insurance discount requires the certificate to be in your name. Contact TAG to pay the transfer fee ($50-$100) and issue a new certificate. Without this documentation, the insurer treats the car as unprotected.

Does the interest rate or term of my loan affect my insurance price?

No. Your premium is based on the vehicle, your driving record, and your location. Lenders request loan details to update their records, not to assess your risk. A 2% loan and a 9% loan cost the same to insure.

What happens if I switch lenders (refinance) mid-policy?

Notify us immediately. We must update the "Loss Payee" to reflect the new bank. If you fail to do this and a total loss occurs, the check might be sent to the old bank, creating legal complications and delaying your settlement.

Is "Gap Insurance" the same as "Replacement Cost"?

No. Gap Insurance (Dealer) only covers the difference between the car's depreciated value and the loan balance. Replacement Cost (Panda7 Endorsement 43) pays to purchase a brand new car. Replacement Cost typically offers stronger protection for a similar or better price.

Industry Trap: The "Dealer Insurance" Upsell

The Trap: The finance manager attempts to sell you "Credit Life" or "Disability Insurance," rolling the cost into your monthly car payment.

The Truth: These dealer-sold policies are often significantly more expensive for the coverage they provide.

The Panda7 Difference: Consult a life insurance broker first. A standard Term Life policy often covers all your debts for a fraction of the cost.

Conclusion: You Are In The Driver's Seat

Bureaucracy thrives on confusion. Lenders use complex terms to make you feel as though you must simply pay whatever is asked.

Now you know the truth. Lender requirements are just a checklist. The Anti-Theft system is a financial tool. The "Small Lender" decline is a routing error that we can fix.

Don't let the paperwork ruin the joy of your new car. Use the tools. Check the boxes. Drive away protected.

Continue Your Research

- To ensure you are getting every other savings opportunity read our guide on Maximize All Available Discounts.

- For a broader look at how to structure your policy for value visit Strategize Coverage for Max Value.

- For a complete playbook of all savings strategies visit our main pillar page: Provide Actionable Savings Strategies.

- Ready to check your lender's acceptance? Get a quote now.

Data Sources & Methodology: Panda7 is committed to radical transparency.

- Source 1: Autorité des marchés financiers (AMF). Regulations regarding mandatory insurance for financed vehicles and QPF No. 1 endorsements.

- Source 2: Groupement des assureurs automobiles (GAA). Data on auto theft frequencies and standard claim settlement procedures for lienholders.

- Source 3: Insurance Bureau of Canada (IBC). Theft statistics and verification of approved anti-theft tracking standards.

- Source 4: TAG Tracking. Pricing models recovery statistics and transfer protocols for secondary owners.

- Source 5: Intact Insurance& Aviva Canada. Underwriting guidelines regarding Approved Lender Lists and high-theft vehicle surcharges.